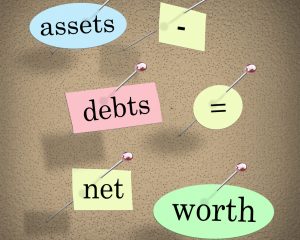

I’ve mentioned how living at home is a great way to save, but many of my friends don’t take advantage of this opportunity. I’ve had friends living at home (making double my income) who have fallen into mountains of credit card debt…and this is without ANY bills! Since I’ve saved around $3,000 in the past three months I thought I’d share my tips for

[ Read More ]